Russian stocks were down sharply across the board in early trading on March 10 after a public holiday, following a crash in oil prices that saw the ruble tumble and global markets plunge.

The RTS index plunged 16 percent at the open before rebounding slightly to be around 13 percent down at 0815 GMT, with shares in oil and gas companies leading the decline.

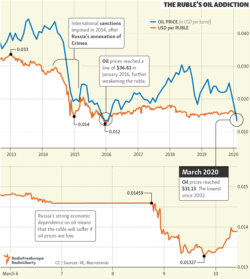

The ruble rose slightly and was trading at around 72 to the U.S. dollar, a day after crashing to a four-year low.

Global stock markets on March 9 suffered their biggest losses in more than a decade in reaction to a fallout between major oil exporters Russia and Saudi Arabia, who are locked in a dispute over output levels.

Russia last week failed to come to a deal with the OPEC oil-exporting group on further reducing output. Saudi Arabia responded with the biggest cut in its prices of the past 20 years in a bid to win market share, leading to a 30 percent plunge in crude to around $31 a barrel.

Markets were already on edge from the economic fallout from the coronavirus outbreak, which has spread to more 100 countries with more than 110,000 cases. The number of deaths worldwide has passed 4,000.

After heavy losses the previous session, European stock markets opened slightly higher, with London's FTSE 100 share index gaining more than 3 percent.

Earlier, Japan's main stock index closed up 0.85 percent and Hong Kong advanced 1.9 percent.

Oil prices also recovered some of their losses, with Brent crude, the standard for international oil prices, rising about 8 percent to around $37 a barrel.

U.S. futures rose following President Donald Trump's announcement he would ask Congress for a tax cut and other measures to ease the pain of the coronavirus outbreak.

Russia's central bank announced on March 10 it would sell foreign currency reserves in a bid to support the ruble.

The decision is aimed at “increasing the predictability of the actions of the monetary authorities and reducing volatility on financial markets amid significant changes in the world oil market,” a central bank statement said.

The previous day, the Russian Finance Ministry said the country’s $150 billion National Well-Being Fund could help the budget withstand a decade of crude prices as low as $25 per barrel.

The oil price drop on March 9 prompted Kazakhstan’s central bank to hike its policy rate to 12 percent from 9.25 percent.

At a government meeting, Prime Minister Asqar Mamin said he was barring state-owned companies from buying foreign currency unless it was required to meet their obligations.